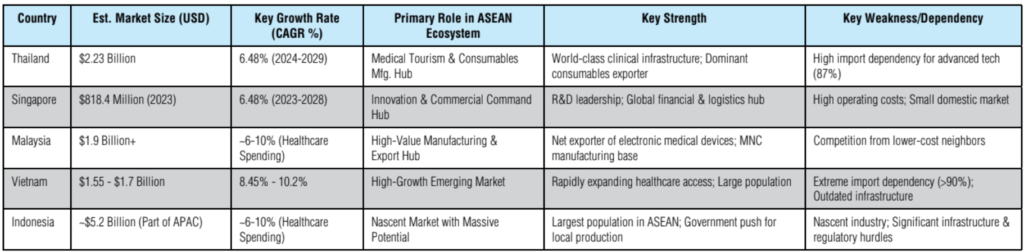

ตลาดอุปกรณ์ทางการแพทย์ในสมาคมประชาชาติแห่งเอเชียตะวันออกเฉียงใต้ (อาเซียน) นับว่าเป็นดินแดนแทบทวีปที่เติบโตรวดเร็วที่สุดแห่งหนึ่งของโลก ขับเคลื่อนโดยปัจจัยพื้นฐานทางเศรษฐกิจมหภาคที่แข็งแกร่ง การเปลี่ยนแปลงทางประชากร และค่าใช้จ่ายด้านการดูแลสุขภาพที่เพิ่มขึ้น ทำให้ตลาดเอเชียแปซิฟิกโดยรวมมีมูลค่าประมาณ 78,250 ล้านดอลลาร์สหรัฐในปี 2024 และมีแนวโน้มว่าจะเติบโตถึง 147,770 ล้านดอลลาร์สหรัฐภายในปี 2031 ด้วยการเติบโตขยายตัวดังกล่าวนี้ ประเทศไทยจึงกลายเป็นตลาดสำคัญและสร้างแบรนด์ให้ตัวเองเป็นศูนย์กลางทางการแพทย์ของเอเชีย ตลาดของประเทศไทยมีมูลค่าถึง 2,230 ล้านดอลลาร์สหรัฐในปี 2024 ซึ่งขับเคลื่อนโดยภาคการท่องเที่ยวระดับโลก ประชากรสูงอายุที่เพิ่มขึ้นอย่างรวดเร็ว และการสนับสนุนจากรัฐบาลทีผ่านโครงการ Thailand 4.0 และ Medical Hub อย่างไรก็ตาม ตลาดของประเทศไทยมีความย้อนแย้งภายในตัวเอง กล่าวคือ ในขณะที่ประเทศไทยเป็นผู้ส่งออกอุปกรณ์ทางการแพทย์รายใหญ่ที่สุดของอาเซียน การผลิตในประเทศกลับมุ่งเน้นไปที่วัสดุสิ้นเปลืองที่ใช้เทคโนโลยีต่ำถึงปานกลาง ดังนั้น ประเทศจึงยังคงต้องพึ่งพาการนำเข้าอุปกรณ์ที่มีความซับซ้อนและมีมูลค่าสูงอย่างมาก ซึ่งจำเป็นต่อการให้บริการดูแลสุขภาพระดับพรีเมียม

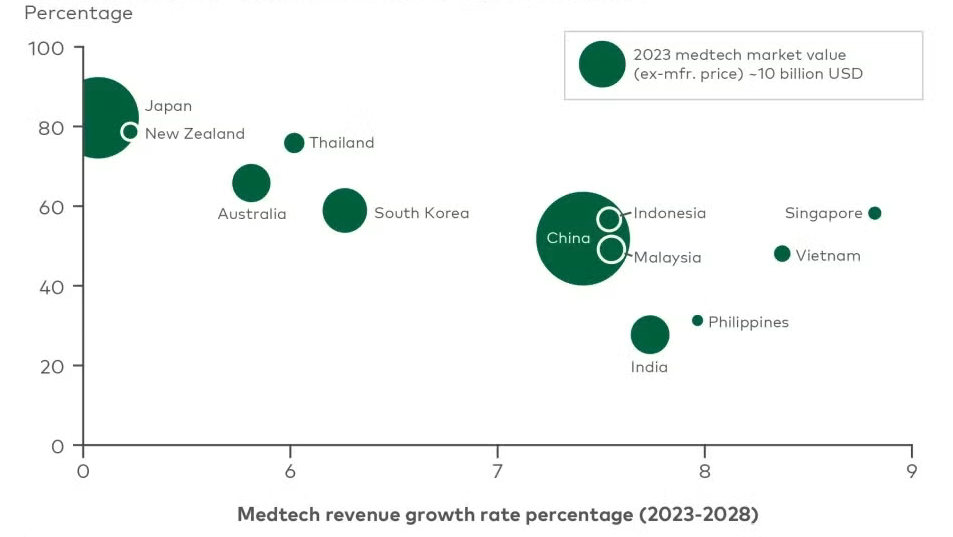

ตามรายงานของ L.E.K. Consulting และ GlobalData เอเชียตะวันออกเฉียงใต้โดดเด่นในฐานะตลาดย่อยที่เติบโตเร็วที่สุดแห่งหนึ่ง คาดว่าการใช้จ่ายด้านการดูแลสุขภาพในประเทศอาเซียนจะเพิ่มขึ้นอย่างมีนัยสำคัญ 6% ถึง 10% ต่อปีจากปี 2022 ถึง 2032 จึงน่าสนใจสำหรับการด้าน MedTech ทั่วโลก ความต้องการสูงเป็นพิเศษในเซกเม้นท์ ตัวอย่างเช่น ตลาดการวินิจฉัยทางการแพทย์ของอาเซียนมีแนวโน้มการเติบโตอย่างแบบพุ่งทะยาน คาดว่าจะขยายตัวจากประมาณ 11.46 พันล้านดอลลาร์สหรัฐในปี 2024 เป็น 18.42 พันล้านดอลลาร์สหรัฐในปี 2028

วิธีทำความเข้าใจตลาดอาเซียนได้ดีที่สุดนั้น คือการมองตลาดอาเซียนแบบระบบนิเวศหลายชั้นที่ประเทศสมาชิกได้พัฒนาบทบาทเฉพาะทางที่ส่งเสริมซึ่งกันและกัน โครงสร้างแบบหลายชั้นนี้มีความหมายอย่างลึกซึ้งต่อกลยุทธ์ขององค์กร โดยมีอิทธิพลต่อการตัดสินใจว่าจะตั้งศูนย์วิจัยและพัฒนา การผลิต และการดำเนินการเชิงพาณิชย์ที่ใด

ระดับที่ 1: ศูนย์กลางนวัตกรรมและบัญชาการ (สิงคโปร์) สิงคโปร์ทำหน้าที่เป็นศูนย์กลางของอุตสาหกรรม MedTech ของอาเซียนอย่างไร้ข้อกังขา ทำหน้าที่เป็นศูนย์กลางระดับภูมิภาคสำหรับการวิจัยและพัฒนา การเงิน และสำนักงานใหญ่ทางการค้า และทำหน้าที่เป็นประตูสู่บริษัทข้ามชาติ (MNC) ที่ต้องการเข้าถึงภูมิภาคเอเชียตะวันออกเฉียงใต้ อีกทั้งเป็นที่ตั้งของศูนย์วิจัยและพัฒนาของบริษัท MedTech ระดับโลกมากกว่า 30 แห่ง รวมถึง Becton Dickison, Alcon และ Hill-Rom ภาคส่วน MedTech มีส่วนสนับสนุนทางเศรษฐกิจที่สำคัญ โดยสร้างผลผลิตการผลิตได้ประมาณ 19,000 ล้านสิงคโปร์ (ประมาณ 14,000 ล้านดอลลาร์สหรัฐ) ในปี 2022 สิงคโปร์เป็นผู้ส่งออกอุปกรณ์ทางการแพทย์เทคโนโลยีสูง โดยส่งออกอุปกรณ์ประมาณ 70% ของอุปกรณ์ทางการแพทย์ที่นำเข้า และเป็นผู้นำในภูมิภาคในด้านค่าใช้จ่ายด้านการดูแลสุขภาพต่อหัว ซึ่งสะท้อนถึงระบบการดูแลสุขภาพขั้นสูงของประเทศ

ระดับที่ 2: แหล่งผลิตและส่งออกที่สำคัญ (มาเลเซียและไทย) ระดับนี้ประกอบด้วยประเทศที่มีศักยภาพในการผลิตที่แข็งแกร่ง\เป็นศูนย์กลางการผลิตระดับภูมิภาคและระดับโลก มาเลเซียประสบความสำเร็จในการวางตำแหน่งตัวเองให้เป็นศูนย์กลางการผลิตที่มีมูลค่าสูง โดยเป็นผู้ส่งออกอุปกรณ์อิเล็กทรอนิกส์ทางการแพทย์เกินดุลการค้าถึง 747 ล้านเหรียญสหรัฐในปี 2023 ขับเคลื่อนจากผลิตภัณฑ์ที่ซับซ้อน เช่น อุปกรณ์วินิจฉัยด้วยไฟฟ้า อุปกรณ์เอกซเรย์ และเครื่องกระตุ้นหัวใจ โดยส่วนใหญ่ผลิตโดยบริษัทข้ามชาติ เช่น Boston Scientific และ Philips ซึ่งทั้ง 2 บริษัทนี้ได้รับประโยชน์จากสภาพแวดล้อมทางธุรกิจที่เอื้ออำนวยของมาเลเซียสำหรับการส่งออกทั่วโลก อีกทั้งยังพัฒนาภาคการท่องเที่ยวเชิงการแพทย์อีกด้วย สำหรับประเทศไทย เมื่อพิจารณาจากมูลค่าแล้ว ประเทศไทยเป็นผู้ส่งออกอุปกรณ์ทางการแพทย์รายใหญ่ที่สุดของอาเซียนและเป็นศูนย์กลางการผลิตและการกระจายสินค้าที่สำคัญสำหรับภูมิภาค อย่างไรก็ตาม ความสามารถในการผลิตของประเทศไทยมุ่งเน้นไปที่สินค้าแบบใช้ครั้งเดียวใช้มีเทคโนโลยีต่ำที่เน้นปริมาณมาก เช่น ถุงมือทางการแพทย์ เข็มฉีดยา และสายสวน ซึ่งใช้ประโยชน์จากวัตถุดิบที่มีอยู่มากมาย เช่น ยางและพลาสติก ไทยยังคงต้องพึ่งพาการนำเข้าเทคโนโลยีทางการแพทย์ขั้นสูงเกือบทั้งหมด

ระดับ 3: ตลาดที่มีการเติบโตสูงและพึ่งพาสูง (เวียดนามและอินโดนีเซีย) มีลักษณะเด่นคือมีประชากรจำนวนมาก เศรษฐกิจเติบโตอย่างรวดเร็ว และอุตสาหกรรม MedTech ที่เพิ่งเริ่มต้น ซึ่งสร้างศักยภาพในการเติบโตมหาศาล คาดว่าตลาดเวียดนามจะเติบโตที่อัตรา CAGR สูงระหว่าง 8.45% ถึง 8.62% จนถึงปี 2030 การเติบโตนี้เป็นผลจากการพลักดันของรัฐบาลที่จะปรับปรุงระบบการดูแลสุขภาพ ซึ่งปัจจุบันอุปกรณ์ทางการแพทย์มากกว่า 90% เป็นการนำเข้า และการผลิตในประเทศตอบสนองความต้องการทั้งหมดเพียง 10% เท่านั้น นี่คือโอกาสสำคัญสำหรับบริษัทต่างชาติที่มีโซลูชันที่สามารถตอบสนองความต้องการด้านการดูแลสุขภาพที่ขยายตัวของประเทศ สำหรับประเทศอินโดนีเซียแล้ว เนื่องจากเป็นประเทศที่มีประชากรมากเป็นอันดับสี่ของโลก อินโดนีเซียจึงถือการเข้าถึงตลาดอินโดนีเซียจึงถือเป็นชัยชนะที่ยิ่งใหญ่ในระยะยาว เพราะอุตสาหกรรมอุปกรณ์ทางการแพทย์ยังอยู่ในช่วงเริ่มต้นและยังต้องพึ่งพาการนำเข้าอุปกรณ์เทคโนโลยีขั้นสูงเป็นอันมาก เช่น เครื่องสแกน CT และเครื่องช่วยหายใจ แม้รัฐบาลได้ส่งเสริมการผลิตในท้องถิ่นอย่างเต็มที่ดังที่เห็นได้จากความร่วมมือล่าสุดระหว่าง GE Healthcare และ Kalbe Farma ในการสร้างโรงงานผลิตเครื่องสแกน CT ในท้องถิ่น ถึงกระนั้นก็ตามช่องว่างด้านเทคโนโลยีและโครงสร้างพื้นฐานยังมีอยู่สูง

สรุป

ภายในปี 2030 แรงกดดันด้านการแข่งขันจะมาก (1) มาเลเซียที่มีความก้าวหน้าทางเทคโนโลยี (2) สิงคโปร์ที่ขับเคลื่อนด้วยนวัตกรรม (3) การผลิตของจีนที่ซับซ้อนมากขึ้น และ (4) การแข่งขันด้านราคา จะส่งผลให้การแข่งขันทวีความรุนแรงมากยิ่งขึ้น กลยุทธที่สำคัญที่สุดของไทยคือการใช้ประโยชน์จากสินทรัพย์ที่เป็นเอกลักษณ์อย่างแท้จริงเพียงหนึ่งเดียวของไทย นั่นคือระบบนิเวศทางคลินิกระดับโลก เพื่อไต่อันดับขึ้นไปในห่วงโซ่คุณค่าทางเทคโนโลยี หากสามารถส่งเสริมความร่วมมืออย่างใกล้ชิดระหว่างโรงพยาบาลชั้นยอดกับอุตสาหกรรมอุปกรณ์การแพทย์ที่เพิ่งเริ่มเติบโต เพื่อขับเคลื่อนนวัตกรรมเชิงคลินิกได้สำเร็จ ก็จะสามารถรับประกันอนาคตที่ยืดหยุ่นและมั่งคั่งได้ แต่หากทำไม่สำเร็จ ก็จะเสี่ยงที่จะเป็นเพียงตลาดทำกำไรสูง แต่ในท้ายที่สุดแล้วต้องพึ่งพาเทคโนโลยีจากต่างประเทศ เป็นเพียงผู้ใช้งานระดับโลกแต่ไม่ใช่ผู้สร้างนวัตกรรมทางการแพทย์ยุคต่อไป

Article by: Asst. Prof. Suwan Juntiwasarakij, Ph.D., Senior Editor & MEGA Tech